The Cash Conversion Cycle (CCC) is a crucial financial metric that measures how efficiently a company manages its working capital. By providing insights into the time it takes for a business to convert its investments in inventory and other resources into cash flow, the CCC allows organizations to optimize operations, improve liquidity, and drive profitability.

In this comprehensive guide, we delve into the intricacies of the cash conversion cycle, covering its formula, real-world examples, and actionable strategies for improvement.

What is the Cash Conversion Cycle?

The Cash Conversion Cycle (CCC), also known as the cash cycle, is a financial metric that quantifies the number of days it takes for a company to:

- Purchase inventory: This represents the process of acquiring raw materials or goods required for production or resale. Companies need to balance purchasing inventory in a way that avoids both overstocking and stockouts, as both scenarios can lead to financial inefficiencies.

- Sell the inventory: The time taken to sell the inventory is influenced by demand, pricing strategy, and market competition. A shorter inventory turnover time reflects effective sales and marketing efforts.

- Collect cash from the sale: After goods are sold, the company must collect payments from customers. This step is crucial for maintaining cash flow and requires efficient credit management policies.

In essence, the CCC highlights how effectively a business converts its resources into cash.

Importance of the Cash Conversion Cycle

- Liquidity Management: A shorter CCC indicates that a company can quickly turn its investments into cash, enhancing liquidity. Liquidity is vital for covering operating expenses, funding new projects, and meeting short-term obligations without relying excessively on external financing.

- Operational Efficiency: By analyzing the CCC, businesses can identify bottlenecks in their operations and take corrective measures. For instance, slow-moving inventory or delays in receivables collection or errors in cash application can be targeted for improvement, streamlining the entire operational process.

- Credit Analysis: Lenders and investors use the CCC to assess a company’s creditworthiness and operational health. A lower CCC often signals a well-managed company with less financial risk, which can lead to better credit terms and investment opportunities.

- Comparative Benchmarking: Companies can benchmark their CCC against industry standards to evaluate performance. This comparison helps in identifying strengths and weaknesses, providing a roadmap for achieving competitive parity or superiority.

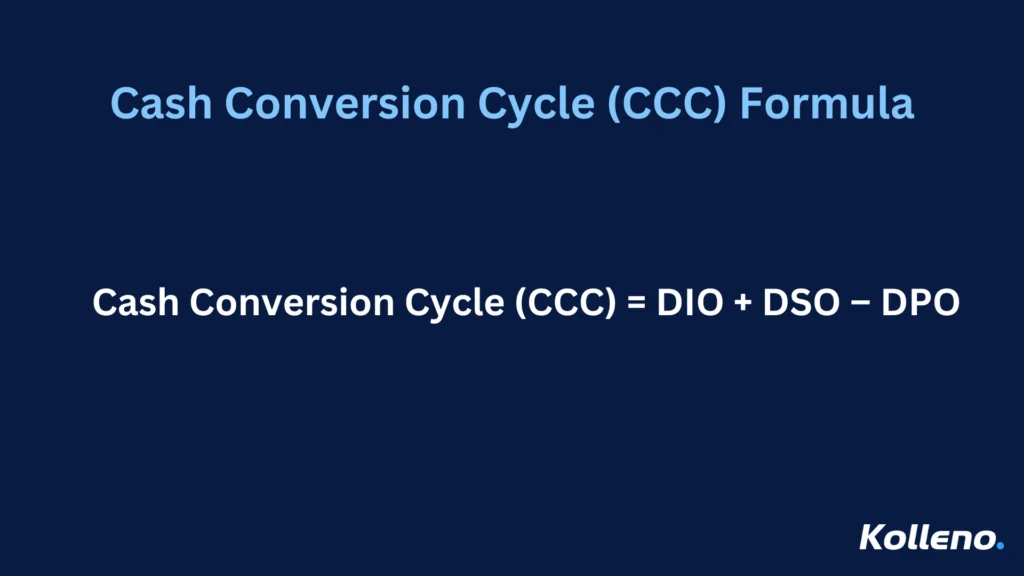

Cash Conversion Cycle Formula

The CCC formula consists of three main components:

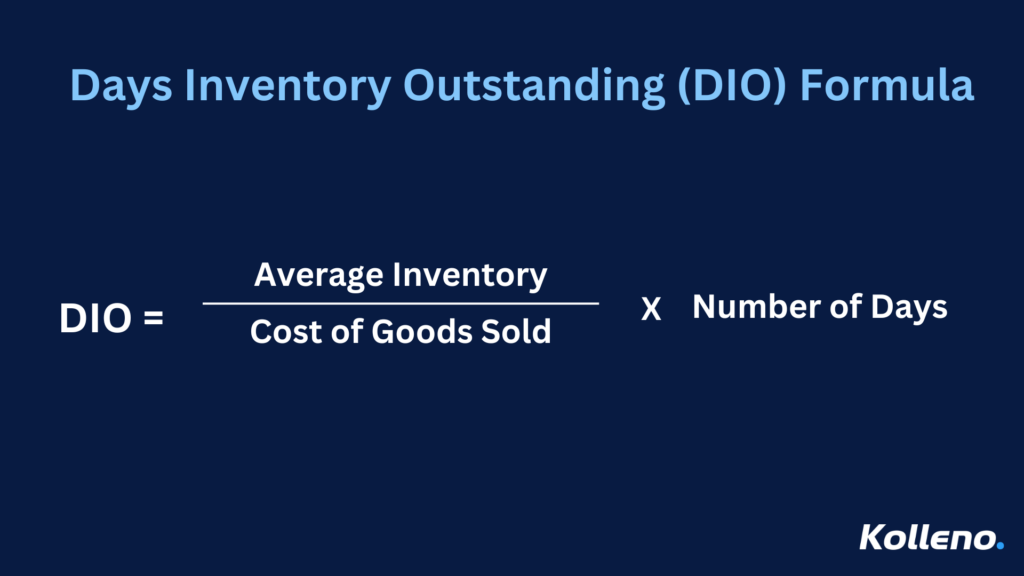

1. Days Inventory Outstanding (DIO):

This measures the average number of days a company takes to sell its inventory.

A higher DIO indicates slow-moving inventory, which ties up capital and storage costs. Conversely, a lower DIO signifies efficient inventory management and quicker turnover.

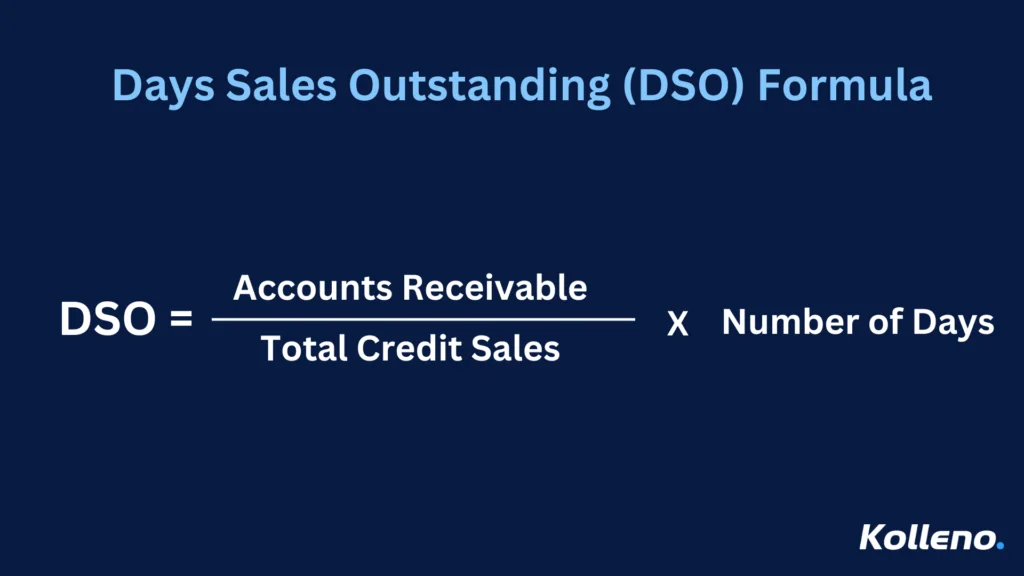

2. Days Sales Outstanding (DSO):

This quantifies the average time it takes to collect payments after a sale.

A high DSO means delays in receivables collection, potentially leading to cash flow issues. Companies aim to keep DSO low by implementing strict credit terms and efficient collections processes.

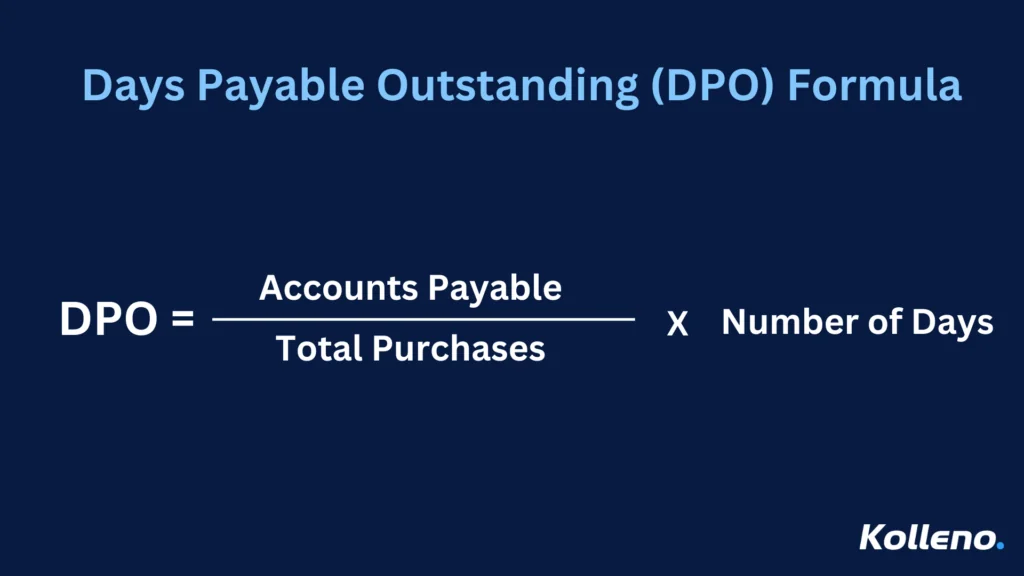

3. Days Payable Outstanding (DPO):

This indicates the average number of days a company takes to pay its suppliers.

A higher DPO allows businesses to retain cash longer, which can be reinvested in operations. However, excessive delays in payments can damage supplier relationships.

Breaking Down the Cash Conversion Cycle

To understand the CCC better, let’s use a hypothetical example:

Example: Company ABC

- Average Inventory: $500,000

- COGS: $3,000,000

- Accounts Receivable: $200,000

- Net Credit Sales: $2,500,000

- Accounts Payable: $300,000

Company ABC has a cash conversion cycle of 53.53 days, indicating it takes approximately 54 days to convert its investments in inventory and receivables into cash.

How to Improve the Cash Conversion Cycle

1. Optimise Inventory Management:

Implementing just-in-time (JIT) inventory systems ensures that inventory levels align closely with current demand, thereby reducing holding costs and preventing waste. For instance, JIT minimizes the need for extensive storage facilities, reducing expenses associated with warehousing. Additionally, demand forecasting—leveraging tools like AI-driven analytics—allows businesses to predict customer demand accurately, enabling them to stock only what is necessary. Supply chain optimization, such as improving relationships with reliable suppliers or adopting agile logistics strategies, also helps in maintaining a steady and efficient inventory flow.

2. Accelerate Accounts Receivable Collection:

Technology plays a pivotal role in streamlining accounts receivable (AR) management and expediting cash collections. Businesses can offer early payment discounts to incentivize customers to pay promptly. For example, providing a 2% discount on invoices paid within 10 days can encourage quicker payments, reducing the average collection period.

AR management and collections software, such as Kolleno, further enhance the efficiency of receivables collection. Kolleno automates invoicing, ensuring timely and accurate invoice generation while eliminating manual errors that could lead to delays. Its comprehensive dashboard provides real-time insights into outstanding invoices, enabling businesses to track overdue payments and send automated reminders to customers. Additionally, Kolleno’s integrated payment platforms simplify the payment process, offering customers flexible options like credit cards, bank transfers, or digital wallets. This streamlined approach not only accelerates cash inflows but also enhances the customer experience by making payments hassle-free.

3. Extend Accounts Payable Period:

Negotiating longer payment terms with suppliers enables businesses to retain cash for extended periods, improving liquidity without increasing operational costs. For example, extending payment terms from 30 days to 60 days can free up cash for other critical investments. Effectively leveraging trade credit, such as building strong relationships with suppliers to secure favorable terms, can also provide additional liquidity. However, it is crucial to maintain transparent communication with suppliers to avoid straining partnerships, which could affect future transactions or product quality

Challenges and Limitations of CCC

- Industry Variability: CCC benchmarks vary significantly across industries. For example, retail companies typically have shorter CCCs compared to capital-intensive industries like manufacturing. Therefore, comparisons must be context-specific.

- Dependency on Accurate Data: Inaccurate financial reporting can distort CCC calculations, leading to poor decision-making. Ensuring the reliability of accounting practices is essential for meaningful analysis.

- Potential Trade-Offs: Extending payment terms may strain supplier relationships, potentially affecting the quality of goods and services received. Balancing cash flow optimization with supplier satisfaction is critical.

FAQs about Cash Conversion Cycle

Q: Can the CCC be negative?

Yes, companies with strong cash flow, like subscription-based businesses, can have a negative CCC. This occurs when they collect payments before fulfilling orders, which provides a significant liquidity advantage.

Q: How often should CCC be monitored?

CCC should be reviewed monthly or quarterly as part of broader financial performance analyses. Frequent monitoring helps in identifying trends and addressing inefficiencies promptly.

Q: What is a good CCC value?

A lower CCC is generally better, but the ideal value depends on the industry and business model. Companies should aim to optimize rather than merely minimize their CCC.

Conclusion

The Cash Conversion Cycle is a vital metric for businesses aiming to enhance operational efficiency and financial health. By understanding and optimizing the CCC, companies can unlock cash flow, reduce reliance on external financing, and achieve sustainable growth.

By focusing on strategies such as inventory optimization, faster receivables collection, and better supplier negotiations, businesses can minimize their CCC and gain a competitive edge in their industry.

Take Action: Start analyzing your company’s CCC today to identify opportunities for improvement and drive financial success.

Kolleno and Atradius hosted a webinar on how to “Enhance your Cash Conversion Cycle and Optimise your Cash Flow” where experts shared practical tips and strategies to improve CCC and Order to Cash.

Looking for a cash application solution? Check out Kolleno.