In today’s fast-paced financial landscape, effective debt management is crucial for businesses looking to optimize cash flow and maintain financial stability. With corporate debt levels continuing to rise, global debt reached a staggering $307 trillion in Q3 2023 according to the Institute of International Finance—organizations need a strategic approach to handling receivables, collections, and compliance. The right debt management software can streamline operations, reduce manual errors, and improve overall financial health.

But with an array of solutions on the market, how do you choose the best one for your business? This guide will break down the key factors to consider when selecting debt management software, ensuring that your organization makes an informed, strategic decision.

1. Understanding Your Debt Management Needs

Before evaluating software options, it’s essential to assess your organization’s specific debt management challenges. Different industries and business sizes require different solutions. Here are some key questions to consider:

- What type of debt are you managing? (e.g., consumer loans, corporate receivables, delinquent accounts)

- Do you need automation for collections and follow-ups?

- Is regulatory compliance a major concern in your industry?

- Are you looking for integration with existing accounting or ERP systems?

Identifying these factors early will help you filter out unsuitable options and focus on solutions that align with your operational goals.

2. Key Features to Look for in Debt Management Software

The best debt management software solutions come equipped with a range of features that help streamline collections, compliance, and reporting. Here are the must-have capabilities:

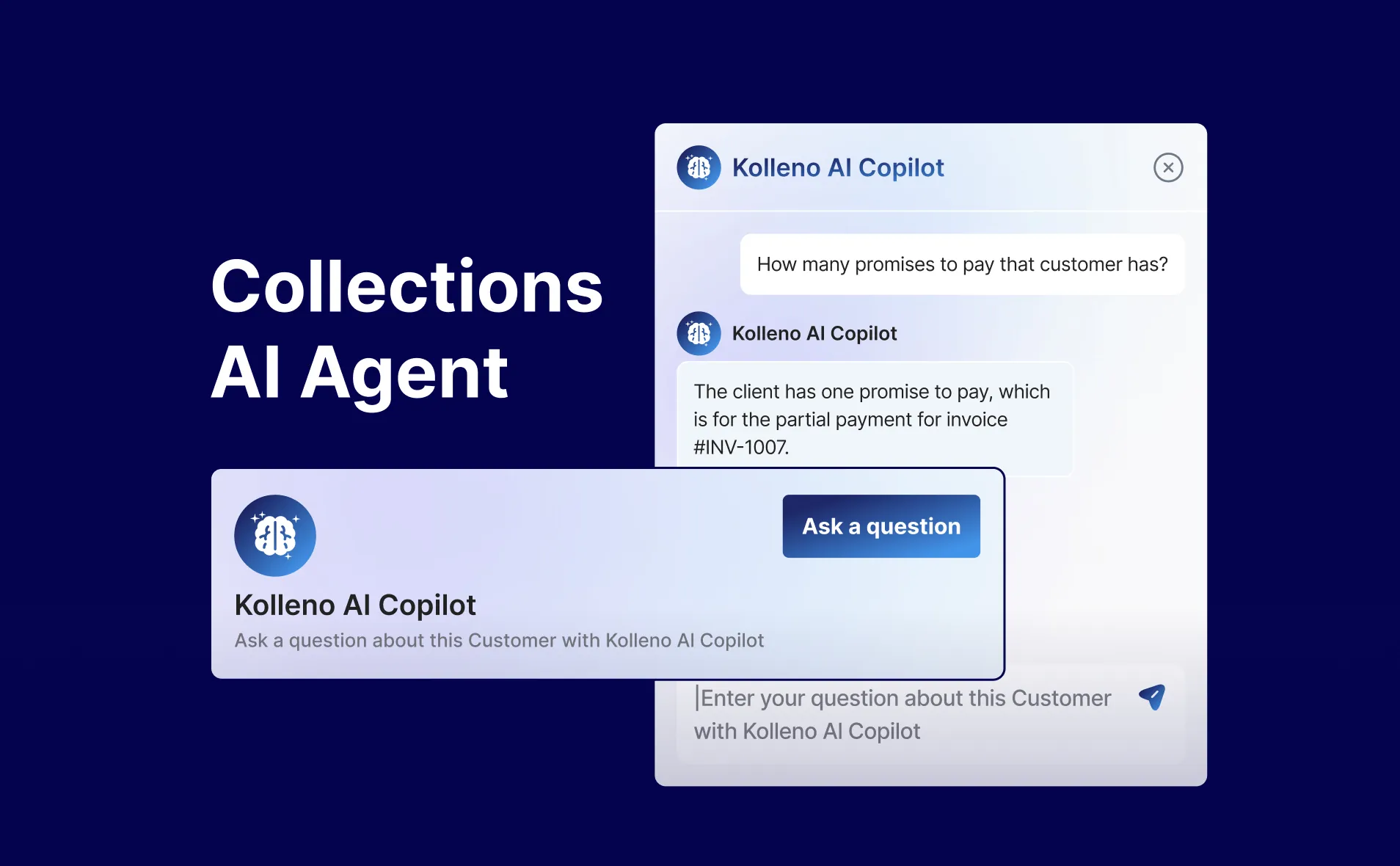

a) Automation & Workflow Optimization

Automation is a game-changer in modern debt management. It helps businesses reduce manual tasks, increase efficiency, and minimize errors. Look for software that offers:

- Automated payment reminders & follow-ups

- Customizable workflows for collections

- AI-driven predictive analytics for risk assessment

A study by McKinsey & Company found that companies implementing automation in financial processes can reduce operational costs by up to 30% while increasing accuracy.

b) Compliance & Regulatory Adherence

Different countries and industries have strict debt collection laws and compliance requirements, such as the Fair Debt Collection Practices Act (FDCPA) in the U.S. or GDPR regulations in Europe. Choose software that:

- Ensures real-time compliance updates

- Includes audit trails and data encryption

- Offers built-in legal templates for collection letters

Non-compliance can lead to hefty fines. Companies failing to adhere to regulations can face penalties exceeding $10 million, as seen in multiple financial institution cases.

c) Integration Capabilities

A well-integrated system eliminates the hassle of switching between platforms. Your debt management software should integrate with:

- Accounting systems (e.g., QuickBooks, Xero)

- ERP solutions (e.g., SAP, Oracle NetSuite)

- CRM platforms (e.g., Salesforce)

Seamless integration enhances workflow efficiency, reducing redundancies and errors.

d) Reporting & Analytics

Data-driven decision-making is critical in finance. Look for a platform that offers:

- Real-time financial dashboards

- Customizable reports on collections and outstanding debt

- AI-powered predictive analytics to forecast defaults

A report by Deloitte indicates that companies leveraging advanced analytics improve debt recovery rates by 20-40% compared to those relying on traditional methods.

e) Multi-Channel Communication

Effective customer communication boosts repayment rates. Opt for software that supports:

- SMS and email notifications

- Call scripting for collection agents

- Self-service portals for customers to view and manage payments

With 80% of consumers preferring digital interactions, according to a PwC survey, having multiple communication channels significantly improves engagement.

3. Evaluating Deployment Options: Cloud vs. On-Premise

Debt management software typically comes in cloud-based or on-premise formats. Understanding their differences is crucial for choosing the right solution.

Cloud-Based Software

- Pros: Lower upfront costs, remote access, automatic updates, scalability

- Cons: Data security concerns, reliance on internet connectivity

- Best for: SMEs and businesses requiring flexibility

On-Premise Software

- Pros: Higher data control, customizable security, no third-party data storage concerns

- Cons: High initial investment, maintenance responsibilities

- Best for: Large enterprises handling sensitive financial data

The global cloud-based financial software market is projected to grow at a CAGR of 11.5% by 2028.

Final Thoughts: Making the Right Choice

Choosing the right debt management software requires a balance between functionality, cost, compliance, and scalability. By assessing your business needs, prioritizing automation, compliance, and analytics, and evaluating vendor reliability, you can make a well-informed decision that optimizes financial performance.

As corporate debt continues to grow, investing in the right debt management solution is no longer optional—it’s a strategic imperative. With the right technology, businesses can enhance cash flow, minimize risk, and maintain long-term financial stability.

Need help navigating the best options for your business? Reach out to industry experts or book a demo from leading software providers to explore the best-fit solution for your needs.