Selling accounts receivable, often referred to as factoring or invoice financing, is a financial strategy businesses use to improve cash flow and maintain operational efficiency. Whether you’re a small startup or a large enterprise, understanding the intricacies of selling accounts receivable can empower you to make better financial decisions.

This comprehensive guide will delve into every aspect of selling accounts receivable, ensuring you have all the information needed to decide if it’s the right choice for your business.

What is Selling Accounts Receivable?

Selling accounts receivable involves transferring outstanding invoices to a third-party financial institution, known as a factor, at a discount. In return, the business receives immediate cash, providing liquidity to meet operational needs.

How It Works

- Invoice Selection: Businesses choose specific invoices to sell based on criteria such as size, customer creditworthiness, and age.

- Engaging a Factor: A factoring company evaluates the invoices and agrees on terms.

- Advance Payment: The factor provides a percentage (typically 70% to 90%) of the invoice value upfront.

- Collections: The factor collects payment directly from the customers.

- Final Payment: After deducting fees, the remaining balance is remitted to the business.

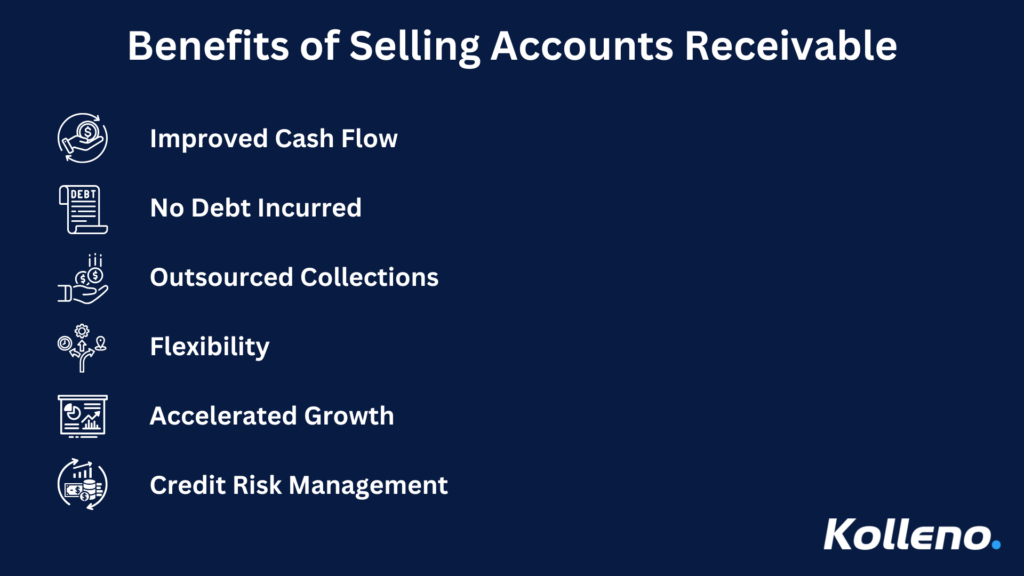

Benefits of Selling Accounts Receivable

1. Improved Cash Flow

Immediate access to cash ensures that businesses can:

- Pay suppliers on time.

- Cover payroll expenses.

- Invest in growth opportunities.

- Reduce financial stress and improve planning for short-term obligations.

2. No Debt Incurred

Unlike loans, selling accounts receivable does not create additional liabilities on the balance sheet. This:

- Improves financial ratios, which can make the business more attractive to investors.

- Eliminates the need for collateral, which is often required for traditional loans.

3. Outsourced Collections

Factors handle the responsibility of collecting payments, reducing administrative burdens and allowing businesses to focus on core activities. This also:

- Saves time and resources that can be redirected toward strategic initiatives.

- Minimizes the potential for strained customer relationships caused by direct collection efforts.

4. Flexibility

Businesses can sell invoices on a need basis without committing to long-term financing agreements. This flexibility:

- Allows companies to adapt to changing cash flow needs.

- Supports seasonal businesses or those with irregular revenue cycles.

5. Accelerated Growth

With quick access to working capital, businesses can:

- Expand into new markets.

- Purchase inventory in bulk to take advantage of supplier discounts.

- Launch marketing campaigns or invest in technology upgrades.

6. Credit Risk Management

When engaging in non-recourse factoring, the factor assumes the risk of non-payment by customers. This:

- Protects businesses from potential losses due to bad debts.

- Enables companies to work with new or less-established clients without fear of non-payment.

7. Improved Financial Predictability

Selling accounts receivable can stabilize cash flow, providing predictable revenue streams. This is especially beneficial for:

- Budgeting and financial planning.

- Meeting fixed expenses such as rent and utilities without delays

Types of Factoring

1. Recourse Factoring

Recourse factoring is a popular option because it typically involves lower fees. However, the business retains responsibility if the customer does not pay the invoice. This type is ideal for companies confident in their customers’ ability to pay on time. Key characteristics include:

- Lower Fees: Reduced risk for the factor results in cost savings for the business.

- Business Responsibility: The business must buy back unpaid invoices or replace them with new ones.

- Common Use Cases: Businesses with reliable customers or those looking to minimize factoring costs.

2. Non-Recourse Factoring

Non-recourse factoring shifts the risk of non-payment entirely to the factor. While this provides added security, it comes at a higher cost. This type of factoring is ideal for businesses that want to mitigate risk. Key aspects include:

- Higher Fees: Factors charge more to compensate for the added risk.

- Risk Protection: Businesses are shielded from bad debts.

- Use Cases: Companies dealing with higher-risk clients or industries prone to payment defaults.

3. Spot Factoring

Spot factoring offers flexibility by allowing businesses to sell individual invoices rather than committing to a long-term agreement. It is suitable for companies with occasional or irregular cash flow needs. Key points include:

- No Long-Term Commitment: Businesses can factor invoices as needed.

- Customizable: Ideal for businesses that want to maintain control over which invoices are sold.

- Higher Fees: Per-invoice fees may be higher due to the lack of a contractual obligation.

4. Whole-Turnover Factoring

Whole-turnover factoring involves selling all outstanding invoices to a factor. This type is often used by larger businesses or those with consistent factoring needs. Key characteristics include:

- Comprehensive Solution: Factors handle all invoices, streamlining operations.

- Lower Per-Invoice Fees: Long-term agreements often result in reduced fees.

- Use Cases: Businesses with high invoice volumes or those seeking to fully outsource accounts receivable management.

5. Maturity Factoring

In maturity factoring, the factor pays the business the invoice amount on the due date, rather than providing an advance. This type works well for businesses that need predictable payment schedules without immediate cash requirements. Key features include:

- Delayed Payment: Payment aligns with the invoice due date.

- Fee Advantages: Often lower fees compared to advance factoring.

- Use Cases: Companies prioritizing cost savings over immediate liquidity.

6. Invoice Discounting

Though similar to factoring, invoice discounting allows businesses to retain control over their accounts receivable. The factor provides funding while the company continues to collect payments from customers. Key points include:

- Confidentiality: Customers are unaware of the factoring arrangement.

- Control Retention: Businesses maintain direct customer relationships.

- Use Cases: Companies that want cash flow benefits without outsourcing collections.

The Process of Selling Accounts Receivable

Selling accounts receivable involves a structured and straightforward process. Here’s a detailed breakdown:

Step 1: Evaluate Business Needs

Begin by identifying the specific financial challenges your business is facing. Are you bridging a temporary cash flow gap, financing a major project, or addressing seasonal revenue fluctuations? Clearly understanding your needs helps you determine the right approach and type of factoring to pursue.

Step 2: Research and Select the Right Factor

Choosing the right factoring company is critical to a successful arrangement. Evaluate potential factors based on:

- Reputation and Experience: Ensure they have a track record in your industry.

- Fee Structures: Compare rates and watch for hidden charges.

- Advance Rates: Understand the percentage of invoice value you’ll receive upfront.

- Customer Service: Opt for factors that provide responsive and transparent communication.

Additionally, consider seeking referrals or reading reviews from other businesses in your sector.

Step 3: Submit Invoices and Documentation

Once you select a factor, provide the necessary documentation, including:

- A list of invoices you wish to factor.

- Payment terms and timelines for each invoice.

- Credit profiles or histories of your customers.

This step ensures the factor can quickly evaluate and approve your invoices.

Step 4: Approval and Funding

After the factor reviews the submitted invoices, they will offer an advance payment. Typically, this is between 70% and 90% of the invoice value. The funding is usually disbursed within 24 to 48 hours, providing your business with immediate cash flow.

Step 5: Communication with Customers

Inform your customers about the factoring arrangement. Factors often handle collections directly, so clear communication ensures a smooth transition. Reassure customers that this process will not disrupt their service or relationship with your business.

Step 6: Collection and Final Payment

The factor collects payment directly from your customers. Once the invoices are paid, the factor deducts their fees and transfers the remaining balance to your account. This step completes the process and allows your business to focus on other priorities.

Potential Drawbacks

1. Costly Financing Option

Factoring fees are often higher than interest rates on traditional loans, which can erode profit margins over time. Businesses need to carefully calculate the net impact on profitability to ensure that the benefits of improved cash flow outweigh the costs of factoring.

2. Customer Perception

Some customers may view factoring as a sign of financial instability, which could impact their trust or willingness to continue business relationships. It’s important to communicate clearly with customers about the arrangement, emphasizing that the decision is a strategic move to improve cash flow rather than a reflection of financial distress.

3. Selective Invoice Acceptance

Factors typically evaluate the creditworthiness of your customers before accepting invoices. This means invoices from customers with poor payment histories or low credit ratings may be rejected. As a result, businesses might not be able to factor all their accounts receivable, limiting the liquidity they can generate.

4. Dependency Risk

Over-reliance on factoring can indicate or exacerbate underlying cash flow issues. Businesses that repeatedly turn to factoring to address cash shortages may need to assess their financial practices, such as pricing, expense management, or collections processes, to develop a more sustainable cash flow strategy.

How to Choose the Right Factoring Partner

Key Considerations

- Industry Experience: Select a factor with expertise in your sector. A factor familiar with your industry’s specific challenges and cash flow patterns can offer tailored solutions. For instance, construction businesses often require unique factoring arrangements compared to retail companies.

- Transparent Fees: Avoid hidden charges that inflate costs. Look for a factoring partner that provides a detailed breakdown of all fees, including administrative costs, discount rates, and penalties for early termination. Clarity ensures you can plan your finances effectively.

- Customer Support: Ensure the factor provides responsive service. A reliable factor will communicate promptly, address any issues, and offer consistent updates on the status of collections and payments. Strong support minimizes disruptions and enhances the overall experience.

- Contract Terms: Review agreements for flexibility and termination clauses. Ensure the contract aligns with your business needs, allowing for adjustments in volume or the option to terminate the agreement without significant penalties if your circumstances change.

Questions to Ask

- What is your advance rate?

- How are factoring fees structured?

- How long does the approval process take?

- What industries do you specialize in?

Frequently Asked Questions about Selling Accounts Receivable

1. Can I sell someone my accounts receivable?

Yes, you can sell your accounts receivable to a factoring company or another third party. This process involves transferring ownership of your invoices in exchange for immediate cash, allowing the buyer to handle collections and receive the payments directly from your customers.

2. Is selling accounts receivable the same as a loan?

No, it’s a transaction where you sell your invoices for cash. It does not create debt.

3. Can any business sell accounts receivable?

Most businesses can, but factors typically evaluate the creditworthiness of your customers and the quality of invoices.

4. How long does the process take?

Approval and funding usually take 1-2 business days.

5. What happens if a customer doesn’t pay?

In recourse factoring, you’ll need to buy back the invoice. In non-recourse factoring, the factor bears the loss.

Conclusion

Selling accounts receivable can be a powerful tool to improve cash flow, reduce administrative burdens, and support business growth. However, it’s essential to weigh the costs and benefits carefully, choose the right factoring partner, and consider its impact on customer relationships.

That said, selling accounts receivable is not the only option. Businesses can also explore accounts receivable software, which streamlines the invoicing and automates collection process, reduces manual errors, and improves cash flow predictability. Such solutions can offer a long-term strategy to optimize cash flow management without selling invoices. Kolleno, for example, is a robust software platform that provides automation and actionable insights, helping businesses efficiently manage their accounts receivable while maintaining full control.

By understanding the nuances of these financial strategies, businesses can unlock new opportunities and maintain financial stability in a competitive market. Whether you’re looking to bridge short-term gaps, fund long-term goals, or automate your accounts receivable process, options like selling accounts receivable or adopting software solutions can help meet your needs.