Struggling to maintain a healthy cash flow? It might be time to take a closer look at your average collection period. This key performance indicator reveals how long it takes to turn your accounts receivable into cash. A longer period could hurt your business, while a shorter one keeps things running smoothly. Read on to learn what the average collection period is, how to calculate it, and how it can help you manage your finances more effectively.

What is the Average Collection Period?

The average collection period refers to the amount of time it takes a business to receive payments from its customers after issuing invoices. In simple terms, it measures how quickly your company turns accounts receivable into cash.

This metric is vital for understanding the efficiency of your collections process. A shorter period suggests that your business is effective at collecting payments promptly, leading to better cash flow and liquidity. On the other hand, a longer period may indicate delays in customer payments, which can strain your ability to meet financial obligations or invest in growth opportunities.

By monitoring your company’s average collection period, you can assess whether your credit policies and payment terms align with your business goals. It also provides insights into how well your accounts receivable department manages outstanding invoices and ensures timely payments from customers.

Why is the Average Collection Period Important?

The average collection period plays a crucial role in maintaining a company’s financial health. It directly impacts cash flow, which is essential for meeting day-to-day expenses, fulfilling financial obligations, and funding future growth.

A shorter collection period indicates that your business is efficient at collecting payments, ensuring enough cash is on hand to cover operations. It also reflects effective credit policies and a well-managed accounts receivable process. On the other hand, a longer collection period can signal inefficiencies in the collections process or issues with payment delays, which might lead to liquidity challenges.

This metric also influences customer relationships. While stricter credit terms can help reduce the collection period, they might deter potential clients. Striking the right balance is key to maintaining healthy cash flow while attracting and retaining customers.

Additionally, the average collection period is an important indicator of short-term liquidity, giving you a clearer picture of your business’s ability to manage its resources effectively. It’s a metric that investors and stakeholders often analyze when evaluating business valuation and operational efficiency.

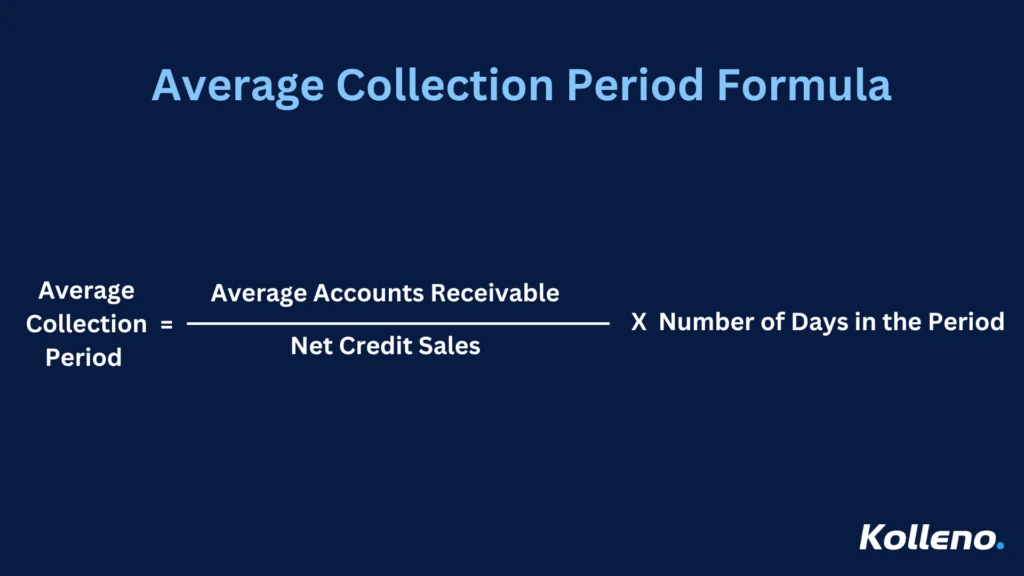

How to Calculate the Average Collection Period

The formula goes as follows:

Average Collection Period = (Average Accounts Receivable / Net Credit Sales) × Number of Days in the Period

Here’s a breakdown of the key components in the average collection period calculation:

- Average accounts receivable: The average balance of your accounts receivable over a specific period. You can calculate this by adding the starting and ending accounts receivable balances for the period and dividing by two.

- Net credit sales: Also known as total net credit sales, this represents the total revenue generated from credit sales (excluding cash sales and any returns or allowances).

- Number of days in the period: Typically 365 for annual calculations or 30 for monthly calculations.

Example Calculation:

Let’s say your business had:

- Average accounts receivable of $50,000.

- Net credit sales of $500,000 for the year.

The calculation would look like this:

Average Collection Period = (500,000 / 50,000) × 365 = 36.5 days

This means it takes your business an average of 36.5 days to collect payment from customers.

The average accounts receivable balance is the midpoint of your accounts receivable over a given period. Calculating this accurately is essential, as it forms the basis for determining your collection efficiency. You can calculate the average accounts receivable balance by summing the opening and closing balances from the balance sheet and dividing by two.

Monitoring this figure regularly helps you track how efficiently your company converts receivables into cash. It also provides actionable insights for improving your collections process if the period is longer than desired.

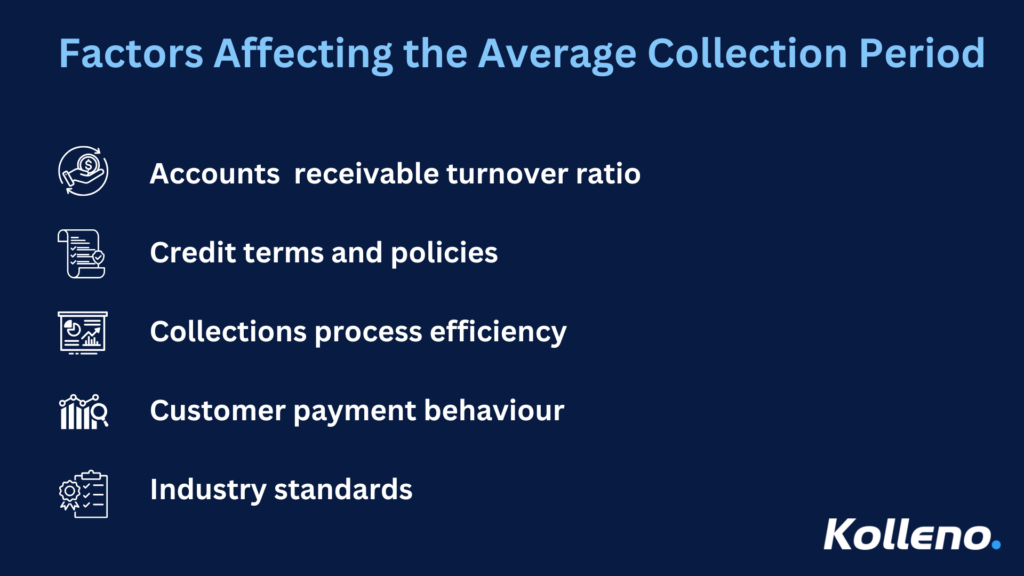

Factors Affecting the Average Collection Period

Several factors influence this metric. Understanding these can help you identify areas for improvement and maintain a healthy cash flow.

- Accounts receivable turnover ratio: This ratio measures how often your business collects payments from customers during a given period. A higher turnover ratio generally indicates efficient collections, leading to a shorter average collection period.

- Credit terms and policies: Your credit terms, such as net 30 or net 60, set the payment timeline for customers. Clear, reasonable terms encourage timely payments, while lenient or unclear policies can lead to late payments and a longer collection period.

- Collections process efficiency: The efficiency of your accounts receivable department plays a critical role. Prompt follow-ups, reminders, and consistent communication with customers ensure payments are collected on time, reducing outstanding invoices.

- Customer payment behavior: Delays in payments from customers can extend your average collection period. Factors like economic conditions, customer relationships, and the reliability of client payments all contribute to this.

- Industry standards: Average collection periods can vary by industry. Comparing your metrics with competitors or industry benchmarks helps gauge whether your collection period is reasonable or needs adjustment.

By addressing these factors, businesses can improve their collections process, minimize late payments, and maintain a lower average collection period.

What is a Good Average Collection Period?

A good average collection period depends on your industry, business model, and customer base. Generally, a shorter period is desirable, as it indicates efficient payment collections and strong cash flow management. However, the ideal range can vary based on specific circumstances.

For most businesses, a collection period that aligns with their credit terms—such as 30 or 60 days—is considered acceptable. If your average collection period significantly exceeds your credit terms, it may suggest inefficiencies in the collections process or lenient credit policies that lead to payment delays.

At the same time, a very short average collection period might not always be favorable. Overly strict payment terms could strain customer relationships or discourage new clients from doing business with you. Balancing efficient collections with maintaining positive customer relationships is essential.

To determine a good average collection period for your company:

- Compare your metrics to industry benchmarks.

- Analyze your cash flow needs and financial obligations.

- Evaluate whether your credit terms are competitive while still promoting timely payments.

Striking the right balance ensures that your business can maintain liquidity, meet financial goals, and foster long-term customer loyalty.

How to Improve Your Average Collection Period

If your average collection period is longer than desired, there are several strategies you can implement to streamline your collections process and maintain a healthier cash flow:

Set clear and competitive credit terms

Review your credit terms to ensure they encourage timely payments while remaining competitive in your industry. For example, offering net 30 terms instead of net 60 can help shorten the collection period.

Strengthen your collections process

Improve the efficiency of your accounts receivable department by implementing regular payment reminders, automated invoicing, and consistent follow-ups. Ensuring your team is proactive can significantly reduce payment delays.

Use technology to track and manage receivables

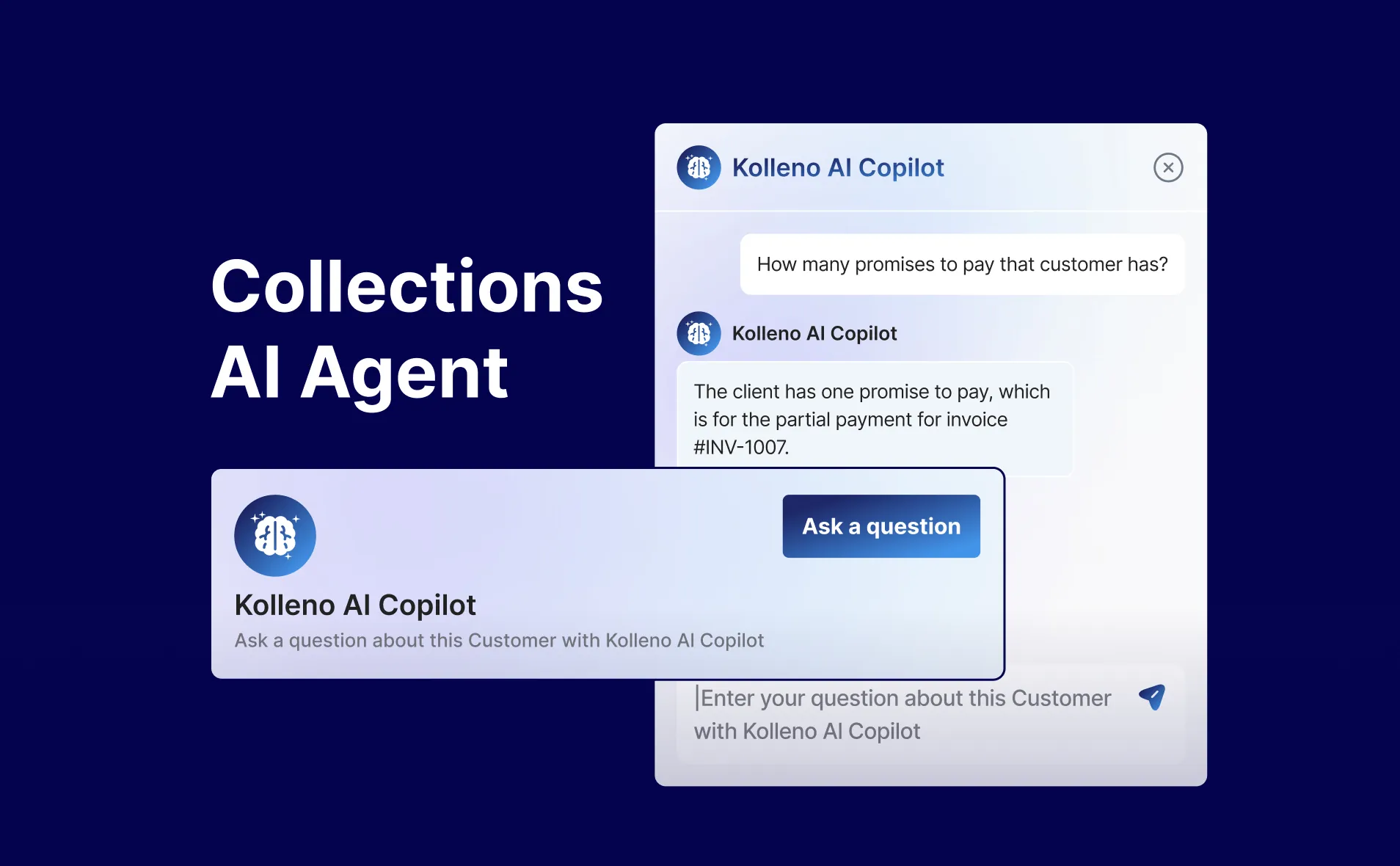

Leverage tools such as an average collection period calculator or accounting software to monitor outstanding invoices and payment patterns. Real-time insights help you spot potential issues before they impact cash flow.

Choosing the right tools can make all the difference in managing your accounts receivable efficiently. Collection software like Kolleno offer comprehensive solutions for automating invoicing, tracking payments, and analyzing customer payment behaviors. With Kolleno, businesses can streamline their collections process and reduce outstanding invoices with ease.

Offer incentives for early payments

Encourage customers to pay before the due date by providing discounts for early payments. For example, a 2% discount for payments made within 10 days can motivate clients to prioritize your invoices.

Build strong customer relationships

Clear communication and positive relationships with customers can lead to better payment practices. Address disputes quickly and work collaboratively to resolve any payment issues.

Reevaluate your credit policies

Assess your credit policies to ensure you’re extending credit to reliable customers. Conduct credit checks on new clients and limit credit for those with a history of late payments.

By taking these steps, you can achieve a lower average collection period, improve short-term liquidity, and maintain a steady cash flow, positioning your business for sustained growth.

Final Thoughts

The average collection period is a crucial metric for evaluating your business’s financial health and operational efficiency. By measuring how long it takes to collect payments from customers, this metric provides insights into your cash flow, short-term liquidity, and the effectiveness of your collections process.

A shorter period signals efficient management of accounts receivable and stronger cash flow, while a longer period may highlight the need for adjustments in credit terms, collection efforts, or customer relationships. By understanding the factors that influence this metric and implementing strategies to optimize it, businesses can ensure they have enough cash to meet financial obligations and invest in future growth.

Looking to streamline your collections? Book a demo to learn how Kolleno can help.